ONBOARDING

Multi-step card offer flow

A multi step card offer flow that address mutliple use cases to fulfilment

.svg)

.png)

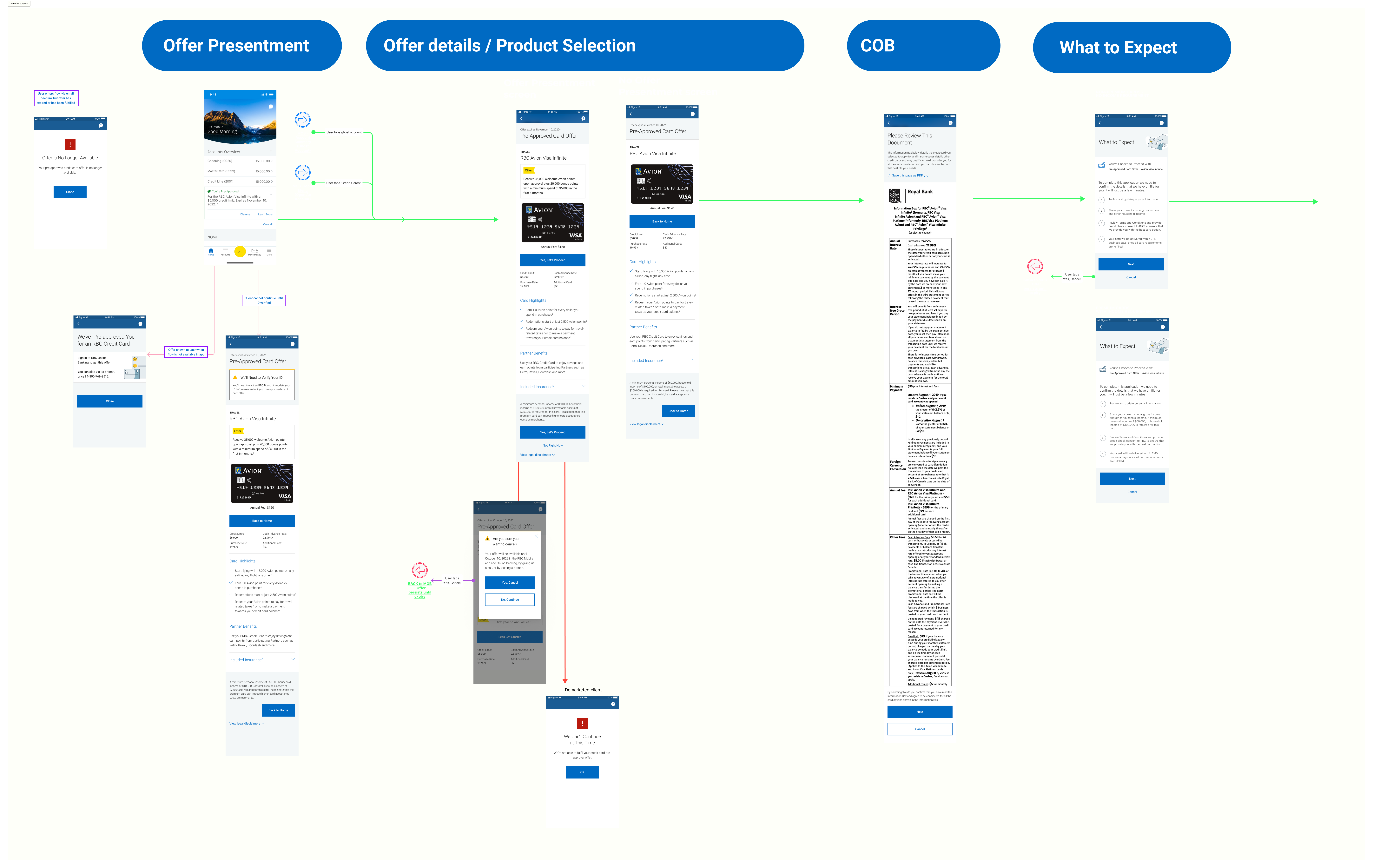

Users felt misled by the term Pre-Approved and as it did not align with their expectations. This was further emphasized by the "Apply" CTA, as users thought that they would simply just have to accept the card and that would be it.

Solution - pre-approved, is a term used across the bank, therefore removing the term was a problem beyond our work. Therefore, emphasis in seeing the value of the card through the content was emphasized. Also the term "apply" was removed and instead messaging around "proceeding" was used.

Users felt underwhelmed by "Using your Rewards". They felt it sounded like marketing and did not bring any tangible benefits that came with the card

Solution - Removed this and replaced with a more tangible benefits, which is mentioned further down.

Users felt after the adjudication screen the following screens seemed unnecessary and just made the flow seem tiresome to actually get the card.

Solution - consolidate some of the screens. In research, users were taken through the Upsell flow, where they were offered an upgraded card. We made it clear they we approved and allowed the user to continue with the original offer.

Users felt they only wanted tangible benefits. Benefits that they had to work towards did not appeal to them.

Solution - Balancing user needs and business needs provided direction in how to remove information but also how to ensure meeting business needs for certain information. A clear separation in the layout allowed offer content to be separated from actual features of the card.

The team expected users to be turned away by the credit bureau check, however, users who were versed in credit in Canada, understood it is part of the process and associated it to RBC looking out for their customers and ensuring they were eligible to take on the proposed credit limit and credit card.

Users were very interested in Partner Benefits, which was the very last screen. This component had a positive reaction from all users and they all mentioned that it was a deciding factor. Users mentioned that they would have liked to have seen it at the very start on the Presentment screen.

Solution - Partner Benefits was mentioned on the first screen. Brought in the Partner Benefits component to the "Approval" screen and changed the layout to a tile visual as Partner Benefits is expected to grow with more Partners over time.

Prior to research, we had a hypothesis around users being put off that they had to apply for an assumed "pre-approved" credit card. The "what to expect" screen, met users expectations and relieved their initial apprehension. The next steps and the idea of the bank simply confirming their information was expected.

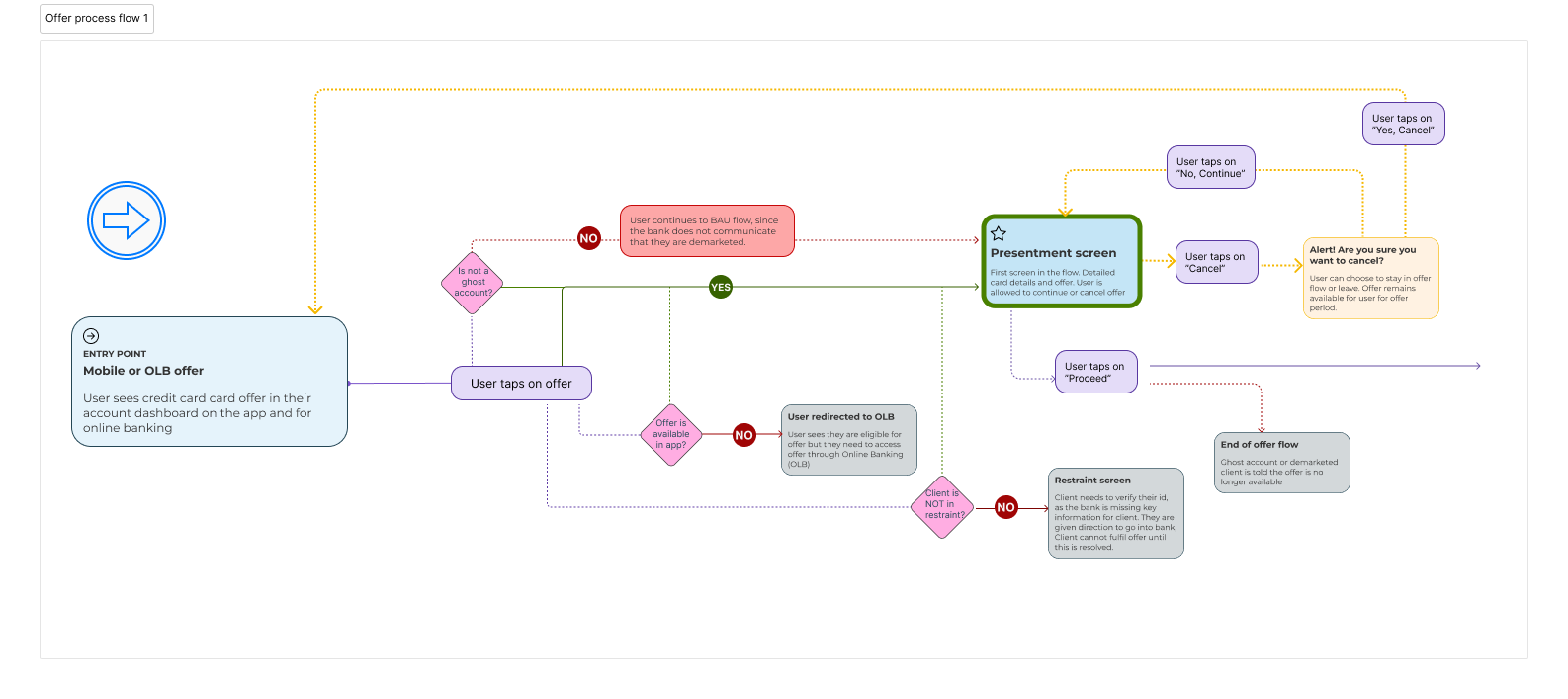

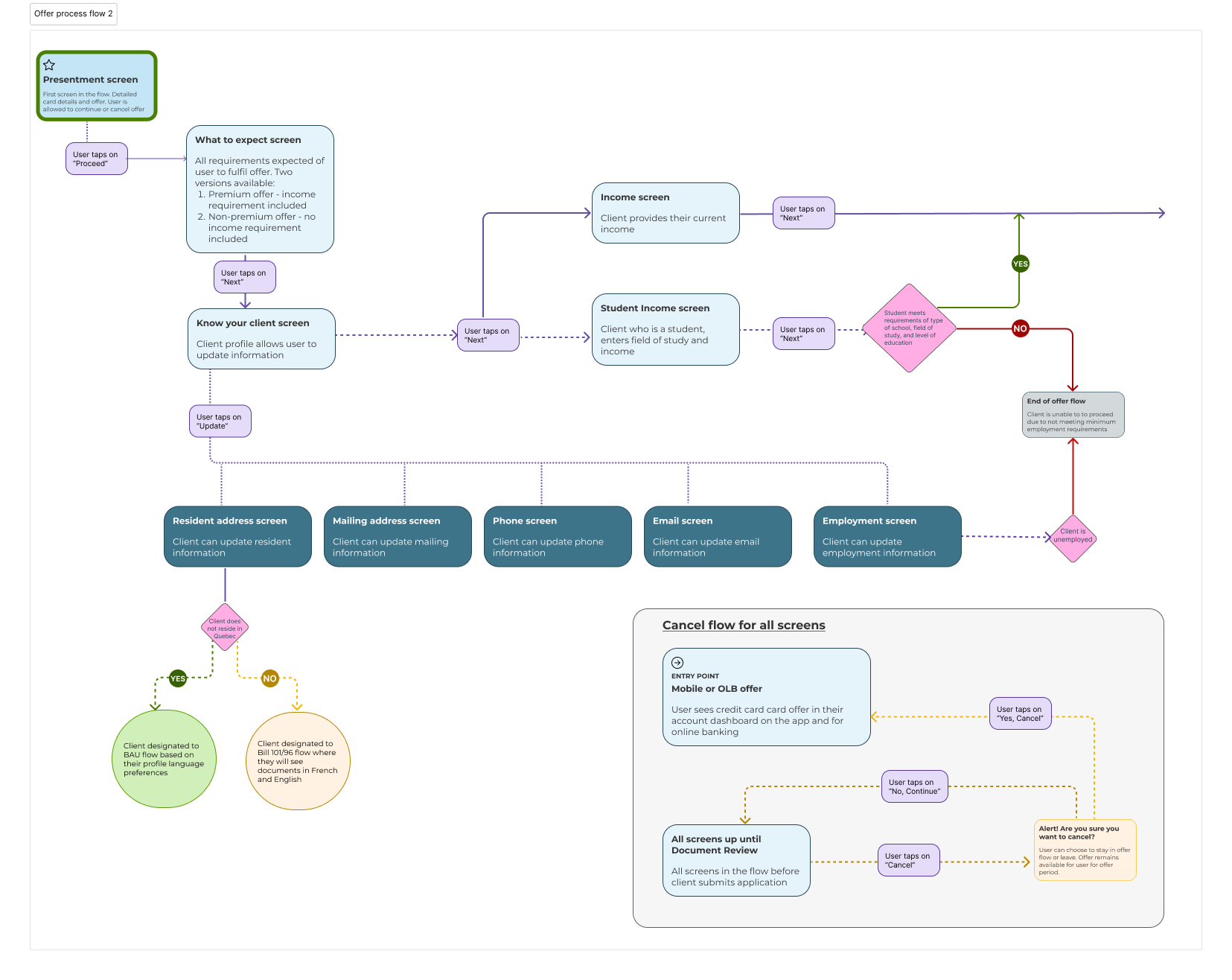

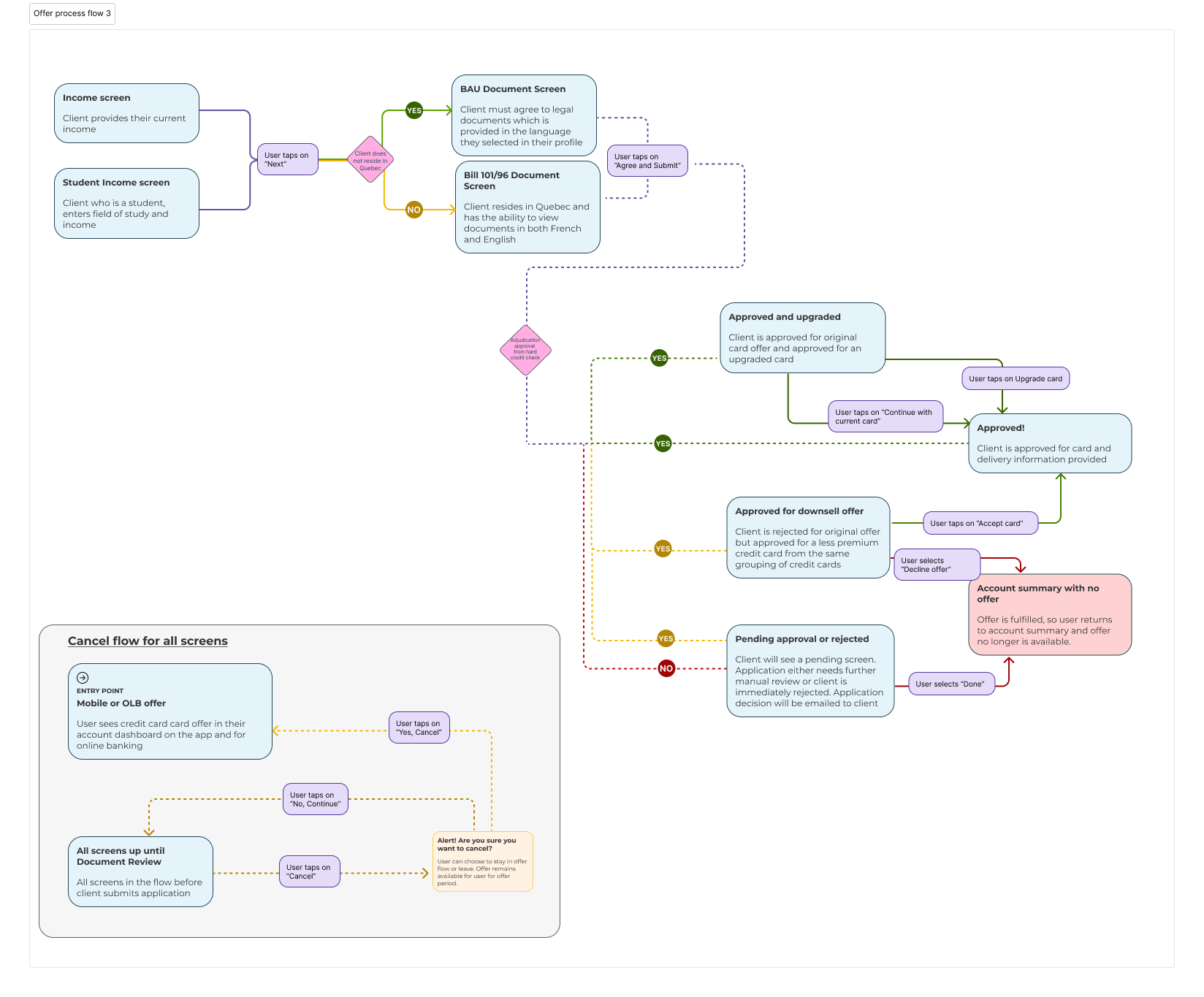

Clients are presented with the credit card offer both in the mobile app and online banking. Below outlines the different outcomes when a user selects the offer from their Account Summary page.

Designed primarily for the mobile app (web view), collaborating closely with the mobile design team to ensure consistency in interactions and visuals across the app.

{kind=link}

{kind=link}

{kind=link}

{kind=link}